And the post-election show interviewing the man behind Arithmetic:

The point, whether prices are involved or not, is that the expectations of individuals add up to an aggregate impossibility. Bubbles are in fact “natural Ponzi schemes”, in which Bernie Madoff’s place is taken by the invisible hand of confusion.

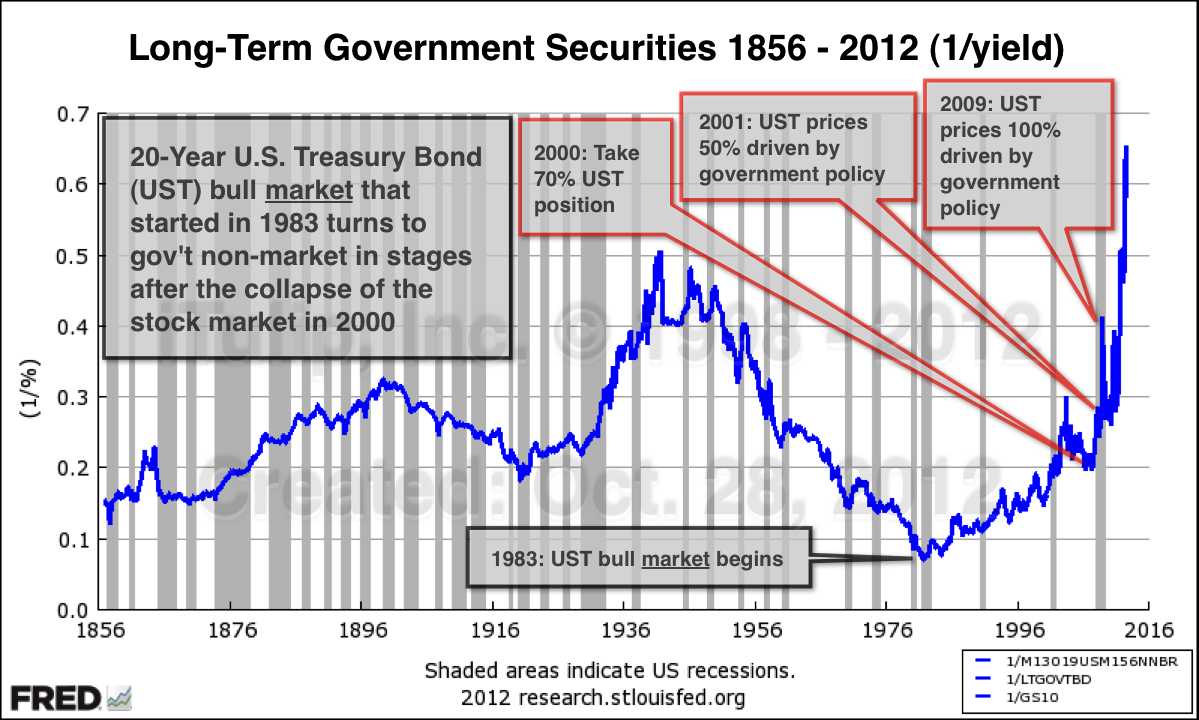

Because the Fed's balance sheet isn't really infinite. It is only infinite for as long as everyone believes that it is.To tie together the thoughts of Krugman and Janszen, individuals expecting bond prices to rise indefinitely, complicated further by the fact that central banks acting as a bidder of last resort -- this situation can continue only as long as it can't.

The logic, if you think about it, is pretty intuitive: with lower interest rates, it makes more sense to hoard gold now and push its actual use further into the future, which means higher prices in the short run and the near future. But suppose this is the right story, or at least a good part of the story, of gold prices. If so, just about everything you read about what gold prices mean is wrong.Brad Delong points this out well in his entry on gold boom:

On this interpretation gold is and always has been a super Treasury bond: a very long duration asset that is or at least is perceived to be "safe" in the sense that its price does not trade at a discount (due to risk and default premia) from a Treasury bond of the same duration but instead trades at a premium.As more certainty emerges on future outlook and expectations, interest rates adjust to them and gold price being sensitive to long-term interest rates will also adjust accordingly.

The Fed stabilized the patient, but the patient remains in the ICU because the doctors cannot agree on the treatment. And of course, the medical directors are stealing the medicine and selling it on the black market. So we have quite the dilemma.

The credibility trap is preventing genuine reform, and the financial system is continuing to distribute the bulk of all new income growth to the wealthiest few, which leaves the vast middle with little discretionary income to fuel demand and organic growth. It is a false equilibrium, but these can last for a decade or more. It really depends on what causes things to change. But change will come.

"many rushed to fill up their tanks Friday night for fear of prices soaring again over the weekend."

People believing crude oil prices heading higher causes crude oil prices to become higher.SFP is a particular type of dynamic process. It is not the truism that people’s perceptions depend on their prior beliefs. Nor is it the truism that beliefs, even false ones, have real consequences. To count as SFP, a belief must have consequences of a peculiar kind: consequences that make reality conform to the initial belief. Moreover, I argue that there is an additional defining criterion. The actors within the process—or at least some of them—fail to understand how their own belief has helped to construct that reality; because their belief is eventually validated, they assume that it had been true at the outset.

Like a lot of people, my insights draw heavily on Diamond-Dybvig (pdf), one of those papers that just opens your mind to a wider reality. What DD argue is that there is a tension between the needs of individual savers — who want ready access to their funds in case a sudden need arises — and the requirements of productive investment, which requires sustained commitment of resources.

America had no major financial panics other than in 1873, 1884, 1890, 1893, 1907, 1930, 1931, 1932, and 1933. Oh, wait. The truth is that returning to gold is an almost comically (and cosmically) bad idea.

Any arrangement that borrows short and lends long, that offers investors claims that are liquid while using their funds to make illiquid investments is a bank in an economic sense — and is potentially subject to bank runs.

To support a stronger economic recovery and to help ensure that inflation, over time, is at the rate most consistent with its dual mandate, the Committee agreed today to increase policy accommodation by purchasing additional agency mortgage-backed securities at a pace of $40 billion per month.

The Committee will closely monitor incoming information on economic and financial developments in coming months. If the outlook for the labor market does not improve substantially, the Committee will continue its purchases of agency mortgage-backed securities, undertake additional asset purchases, and employ its other policy tools as appropriate until such improvement is achieved in a context of price stability. In determining the size, pace, and composition of its asset purchases, the Committee will, as always, take appropriate account of the likely efficacy and costs of such purchases.In addition to the ongoing Operation Twist (extending duration of the Fed's portfolio), the Fed has also decided to purchase agency-backed MBS for the tune of $40 billion a month, until the labor market improves. They have not clearly specified the target they are looking at, which is worrisome.

My theory is this: our depression is not a problem of insufficient demand. It is systemic; most prominently and immediately financial fragility, financial zombification, moral hazard, and excessive private debt, alongside a huge number of other long-term systemic problems.What if the Fed and the market monetarists are completely wrong? What if all central banks engage in a competitive devaluation strategy and these currency wars precipitate into trade or real wars? Here is Ed Haddas from Reuters:

It is a dangerous way to conduct monetary policy. A large trade surplus may have helped create jobs in China, but the accumulated funds helped finance the asset bubbles which eventually popped, leading to the current global malaise. The Fed’s previous rounds of quantitative easing just might have helped the American economy, but they almost certainly pushed up commodity prices, which stimulated economic and political tension in many poor countries. They also spawned ill will among the central bankers who were forced to deal with collateral damage from the U.S. war against domestic financial disorders.

When the energy level of the self-boosting system overwhelms centripetal forces, the system snaps like a broken chain, releasing the surplus energy most destructively. This is the substance of every crack-up boom. Like Mises, I also object to the use of the word hyperinflation, albeit for a different reason. It suggests that the phenomenon is linear and follows the laws of the Quantity Theory of Money. The more money is printed, the higher do prices go. However, we are here facing highly non-linear phenomena. Our economy is torn to pieces by runaway vibration. We are victimized by the self-destruction of the monetary system subjected to oscillating money-flows boosted by the resonance of fluctuating interest rates resonating with fluctuating prices.

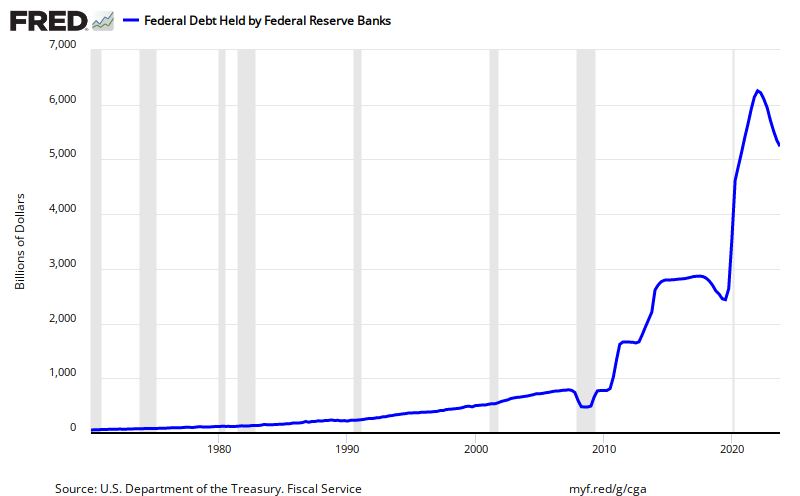

The USG today is spending $3.6B more than it is taking in, each and every day. That's a big mess of dollars flooding out of the USG. $1.5B per day is flooding outside of our zone while $2.1B is staying right here on our front lawn. This is all flow. It is ongoing and unstoppable. And it all must be mopped up by someone. And by someone, I mean either the foreign sector, the domestic private sector or the Fed buying up US Treasuries. $3.6B per day, an unstoppable, unending broken water main gushing out dollars. Marginal flow!

Don't be fooled by the misdirection. QE, twist, whatever; it's not about interest rates or helping the economy recover. It's 100% about disguising and managing this uncontrollable, unstoppable mess. It's more like a broken sewer line than a water main now that I think about it.

Sure, the Fed needs to keep interest rates from rising. Because what happens when interest rates rise? The value of the entire $35T bond market starts to collapse and bond holders panic. The Fed doesn't want that, so don't bet on them letting interest rates rise. But as I said, I'm not worried about the stock of dollars. I'm worried about this broken sewer line we call the federal budget deficit which means no one has to sell a single bond. In fact, someone has to continuously buy $3.6B more each and every day, including weekends and holidays.

The USG thinks (and truly believes) that the key to rejuvenating the US economy is trashing the dollar as a short cut to increasing exports (reducing the trade deficit). But what it can't see (nor anyone that focuses solely on the monetary plane for adjustment) is that the huge trade deficit the USG wants to quit is actually its own heroin fix. This is a deadly combo for the US dollar.The key point to take away is that Budget Deficit and Trade deficit are inter-related in the sense that government spending towards goods and services increases our imports, therefore worsening the trade deficit.